Introduction

The spillover effects of proximity to external features in the existing environment

Changes in the property value of a LEED or Energy Star certified building

Problem statement

Methodology

Study area

Analytical approaches, data sources, and variables

Definition of the level or coverage of LEED certification

Defining neighborhood areas based on walkable distance

Definition of the neighborhoods and sub-neighborhoods of the LEED and/or Energy Star certified office buildings

Redefining sub-neighboring buildings for the median market value of the buildings in each sub-neighborhood

Overlapping areas of each sub-neighborhood of LEED and/or Energy Star certified office buildings

The proximity to a subway entrance for each building in the sub-neighborhoods

Findings

Geographical results

Statistical approaches

Conclusions

Introduction

Green certified buildings are rapidly gaining acceptance, and the public recognition of green building certification is expected to advance routine evaluations of sustainability [1, 2]. Researchers generally examine the sustainability of LEED or Energy Star certifications in terms of the triple bottom line of sustainability. First articulated by Spreckley in 1981 [3], this looks at not only the contributions to environmental conservation issues and the quality of human life signified by LEED or Energy Star certification, but also the associated economic benefits, including socio-economic benefits. Kerstens et al. [4] and Suh et al. [5] agreed that the 3Ps (People, Planet, and Profit) are interconnected, emphasizing the importance of ensuring that individual residents and their immediate neighborhoods share in the profits of such developments to support mutual growth. This study therefore sought to investigate the diffusion of the economic spillover effect of LEED and/or Energy Star certified office buildings in New York City (NYC) for their immediate neighbors and the surrounding local community in order to determine whether this is indeed a win-win approach, thus satisfying the triple bottom line of sustainability element of LEED and/or Energy Star certification.

The spillover effects of proximity to external features in the existing environment

Property values are determined by demand and supply in a real estate market and can be measured in terms of rental rates, unit sales prices, resale value rates, and occupancy or vacancy rates [6, 7]. In general, property values are determined by tangible and intangible environmental features, such as changes in the property values of other buildings in the neighborhood or in the same community [6, 8]. Several researchers have reported that economic changes in property values in a specific area that had undergone a significant change in the neighborhood environment often exhibit a correlation with the market value of a particular building [9, 10, 11, 12, 13, 14, 15, 16, 17]. Nelson [18] concluded that airport infrastructure systems had a negative impact on residential properties located around the airport due to the high noise levels, while Weinberger [9] found proximity to light rail transit had a positive impact on both residential and commercial property values in his research area. Lin et al. [12] showed that the negative impact of an intangible external environmental feature, a foreclosure, on residential property values in the immediate vicinity decreased with increasing distance, becoming insignificant for properties more than 0.9 km (0.55 miles) away. Aydin et al. [13] found the greatest positive spillover effect was also within a 0.5-mile radius of the district’s boundaries, after which the positive spillover effect started to fade. Chang and Chou [14], Suh et al. [16], and Suh et al. [17] demonstrated that nearby green buildings can have a positive impact on the surrounding area, possibly by boosting the community’s reputation or improving the local economy.

The proximity of an individual property to external environmental features is likely to be important because these external environmental features will exert a spillover effect on the economic value of a property. Gelfand et al. [19] contended that the qualities of a residential building and its proximity to amenities served as proxies for this spillover effect. Tandon [20] also highlighted the importance of proximity, explaining that “If the house price is influenced by the location factors then there is a strong prospect that neighboring houses are also influenced by the same location factors” (p. 31). Any changes in the property value of a building would thus be expected to have a knock-on effect on neighboring buildings and could become one of the determinant factors influencing buyers in the local real estate market. Geographical changes could potentially also play a role in establishing the values of comparable buildings in the same neighborhood under similar conditions [21]. As Tandon [20] noted, “The closer the neighbors are in space, the greater is the price influence on the subject property … Housing transactions are also known to be influenced by the prices of recently sold houses in the neighborhood” (p.29 and p.31). Jeong [21] agreed, pointing out that the market value of neighboring buildings included every surrounding external environmental condition, and the market value of neighboring buildings should therefore be included among the external environmental features of the subject property.

Changes in the property value of a LEED or Energy Star certified building

Researchers have examined the economic impact of LEED or Energy Star certification on a building by measuring changes in the certified building’s rental rates, occupancy rates, and resale value rates, as shown in Table 1.

Table 1.

Comparison of LEED and Energy Star certified buildings and comparable non-certified buildings

| Property type | Rental rates | Occupancy rates | Resale value rates | |

|

Miller et al. [23] |

All types of property |

LEED was about 20% (2006; 1Q)-50% (2006; 3Q) higher Energy Star was about 0.5% (2005; 1Q)-9% (2007; 2Q) higher |

LEED was about 0% (2006; 3Q)-4.7% (2005; 4Q) higher and 0.7% (2006; 2Q) lower; Energy Star was about 1% (2005; 2Q)-3.5% (2008; 1Q) higher |

LEED was about 9.9% lower; Energy Star was about 5.3% higher |

|

Eichholtz et al. [24] |

Office property |

LEED was 6% higher; Energy Star was 6.5% higher | LEED or Energy Star were 2.35% higher |

LEED was about 11% lower; Energy Star was about 12.9% higher |

|

Wiley et al. [22] |

Commercial property |

LEED was 15.2-17.3% higher; Energy Star was 7.3-8.9% higher |

LEED was 16.2-17.9% higher; Energy Star was 10-11% higher |

Wiley et al. [22] found that Energy Star certified buildings in the U.S. enjoyed a 7.3 to 8.9 percent premium on their rental rates, and there was at least a 15 percent premium on the rental rates for LEED certified buildings. Miller et al. [23] and Eichholtz et al. [24] agreed, reporting that the resale values of LEED or Energy Star certified buildings were higher than those of non-certified buildings; Miller et al. [23] also found the occupancy rates of LEED only and Energy Star only certified buildings tended to be higher than those of non-certified buildings. LEED or Energy Star certification can thus have a positive effect on the metrics of a building’s property value, and this positive impact could encourage a synergistic effect between a LEED or Energy Star certified building and its surrounding neighborhood through the spillover effect.

Problem statement

Tandon [20] and Jeong [21] pointed out that economic factors could potentially play a role in setting the prices for comparable buildings in the same neighborhood in a real estate market. In particular, there is a relationship between proximity to the subject property and the spillover effect it creates for the surrounding neighborhood [12, 13]. The studies discussed above in the literature review examined the impact of typical external environmental features on the market value of properties; thus, this study investigates the impact of LEED and/or Energy Star certificates on three different neighborhood areas, treating their proximity to certified buildings as an external environment that affects the market value of neighboring properties. The hypothesis guiding this study thus posits that the various economic spillover effects of a LEED and/or Energy Star certified office building on the buildings in its vicinity depend on their proximity to the LEED and/or Energy Star certified office building. Therefore, this research examined the spillover effect for neighborhood buildings with different proximities to the LEED and/or Energy Star certified office building.

Methodology

This research utilized two methodologies, a geographical analysis and a statistical analysis. For the purposes of this research, the distribution of LEED and/or Energy Star certified office buildings, the buildings in their neighborhood areas, and the synchronization of market value data for each building were determined by the geographical analysis, and the correlations between independent variables and dependent variables revealed by the statistical analysis, with the correlations being validated by the statistical analysis. Details of the research process are presented below.

Study area

NYC is one of the most vibrant cities in the US. The highest density of LEED and/or Energy Star certified buildings in the nation is in Manhattan and NYC’s five boroughs are home to the second largest number of LEED certified buildings of any metropolitan area and the fourth highest number of Energy Star certified buildings. About 80 percent of the city’s LEED certified buildings are in a single borough, Manhattan, along with 90 percent of its Energy Star certified buildings.

Analytical approaches, data sources, and variables

Geographical and statistical approaches were applied to analyze the spillover effects of LEED and/or Energy Star certified office buildings on buildings in their sub-neighborhoods. The geographical method established the spatial characteristics of the LEED and/or Energy Star certified office buildings and their sub-neighborhoods using a “Multiple Ring Buffer’ to enhance the accuracy of the buildings’ geographical locations. The two statistical methods utilized, namely descriptive analysis and regression analysis, required two different data sets. Information on building characteristics and the geographic information for the LEED and/or Energy Star certified office buildings and the buildings in their neighborhood were provided by NYC’s Department of City Planning (DCP), the US Green Building Council (USGBC), and the US Environmental Protection Agency (USEPA) to ensure accuracy and maintain the consistency of the information in the data. The regularly updated basic geographical data for the Geographic Information System (GIS) was provided by NYC’s DCP. The estimated market value is commonly represented by the price of a transaction that transfers a property’s ownership from a seller to a buyer in a competitive and open market under stable conditions [25, 26]. Although Cypher and Hansz [27] and Aydin et al. [13] pointed out the flaws in estimated market value, Aydin et al.[13], Suh et al. [17], Kim and Son [28], Matthews [29], Dermisi [30], and Zhang [31] argued that estimated market value provides a useful approximation for future property buyers, given the limited number of actual transactions or sales, along with the difficulty of obtaining actual transaction price data sets; they also showed a valid correlation between actual sales prices and estimated market values. Furthermore, NYC’s Department of Finance (DOF) makes every effort to develop realistic estimated market values, annually estimating the market value of every building in NYC to minimize discrepancies between the estimated market value and actual transaction prices and adopting different approaches where necessary to take into account internal and external environmental conditions. The market value data set was collected from the DOF website for the period from 2009 through 2015 and via a Freedom of Information Law (FOIL) request. Although the data sets for LEED and Energy Star certifications were available for the period from 2003 through 2013, the market value data sets ran from fiscal year (FY) 2007 through FY 2015. The data analyzed for the current study therefore covered the period FY 2007 to FY 2013 where both datasets were available (Table 2).

Table 2.

Research variables and the corresponding data sources

Lee [32] recommended the hedonic price model as one of the most appropriate ways to analyze environmental values using cross-sectional data. Can [33], Lee et al. [34], and Gibbons et al. [35] concurred, suggesting that it provides a useful way to find the effect of neighborhood, including both socio-economic characteristics and physical features. It has also been widely used to analyze correlations in real estate markets because it allows researchers to select a group of characteristics from among the multiple heterogeneous characteristics that affect the property value directly or indirectly to serve as appropriate independent variables in the hedonic price equations for their research [9, 28, 36, 37, 38, 39]. The linear mixed effect model (LMEM) is often applied to examine changes in the market value of neighborhood characteristics over time, especially for analyzing repeated measure data and cross-sectional data in multiple research fields [40, 41]. In this study, the numerical models produced by these statistical methods were validated using the Log-likelihood Ratio Test (LRT), which indicate the fitness of numerical models by comparing them with the null model.

Definition of the level or coverage of LEED certification

Once Energy Star certification is achieved, if building stakeholders wish to maintain that certification it must be renewed annually through a re-evaluation that is based on the building’s performance during the certified year. In contrast, LEED certification does not require this re-evaluation for its annual renewals; it is also possible for a LEED certification to be re-achieved or its coverage to be extended from part of a building to the whole building. In the screened population in this study, 15 LEED certified office buildings achieved more than two LEED certifications by enhancing their initial LEED certification levels, either by extending their current LEED certification coverage from part of the building to the whole building or adding another LEED certification for a specific part of an active LEED certified office building to that for the whole building. For this study, the coverage and level of a LEED certified office building that achieved multiple LEED certifications with different coverages and higher LEED certification levels was defined based on the level of LEED certification coverage and the hierarchy of LEED certification level. LEED certification for a whole building took precedence over LEED certification for part of building, after which the higher level of LEED certification was given priority when defining the level of a LEED certified office building with more than two LEED certifications, as shown in Table 3.

Table 3.

Defining the coverage and level of LEED certification for multiple achieving LEED certified office buildings

Defining neighborhood areas based on walkable distance

In the real estate market, external features such as demographic factors are major determinants in a building’s existing environment because they have a significant effect on both the target property and surrounding properties [25, 28]. O’Sullivan [7] contended that demographic factors are important for office property values, with a higher population density supporting higher rental rates for office buildings because face-to-face meetings involve spending time and money to service providers’ employees. They suggested that walkability might be a core factor for buyers or tenants, especially the proximity between their workplaces and living spaces. Leinberger [42] agreed, reporting that home seekers showed a willingness to pay more for housing that was in closer proximity to their workplaces. Other researchers have also quantified proximities to destinations that were favored by commuters, indicating walkable distances of between 0.2 miles and 0.3 miles or between five and ten minutes [25, 43, 44, 45]. The new metric “WalkScore” was introduced to provide an online score for residential property values that takes into account their proximity to different types of amenities such as NYC’s Metropolitan Transportation Authority (NYC MTA) subway, which is a key external environmental feature in the city [46]. Commuters foster more livable communities through their contacts with local businesses as they walk through their neighborhoods on their way to and from work [47, 48].

Definition of the neighborhoods and sub-neighborhoods of the LEED and/or Energy Star certified office buildings

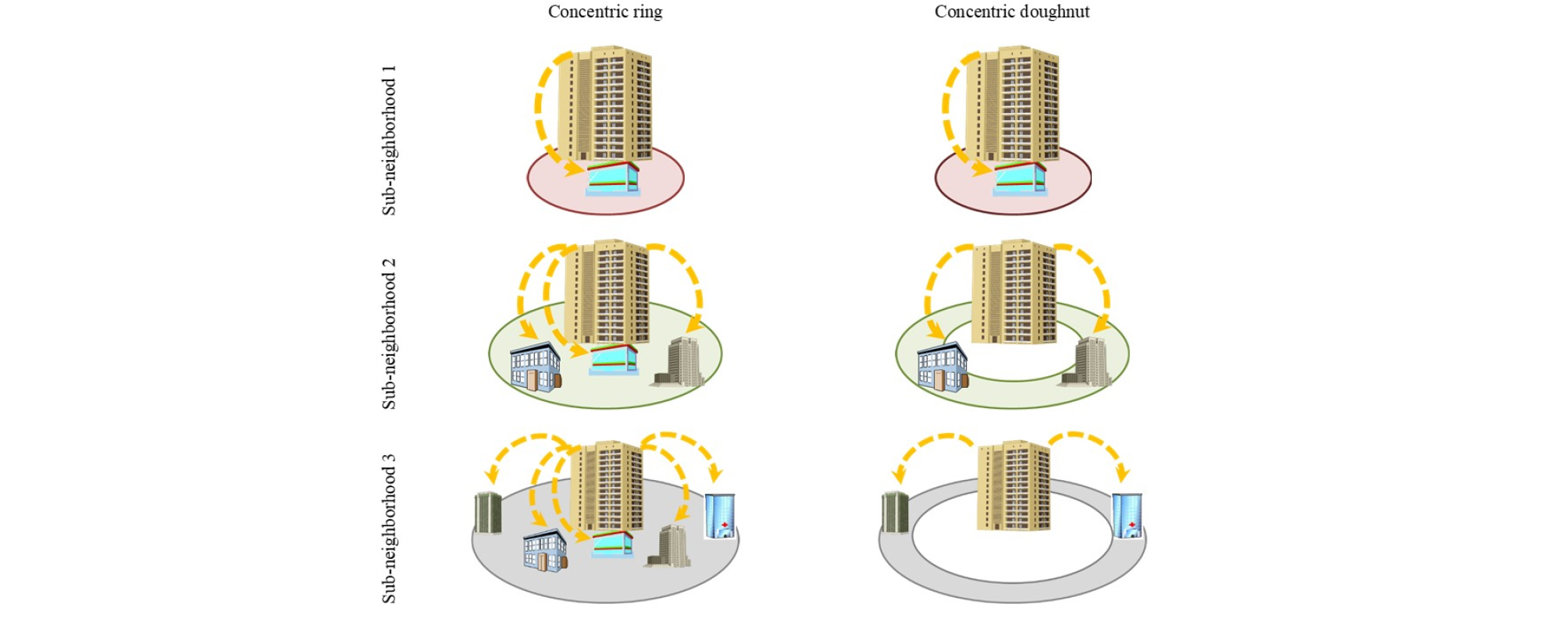

The neighborhood of each building was defined in terms of the standard measure of walkable distance in NYC due to the importance of this factor for local property values as an external feature in the existing environment. Each sub-neighborhood has homogeneous external features in its existing environment, with the only significant variation being its proximity to the LEED and/or Energy Star certified office building. Every building in the study area is located within a 15-minute walk of a subway entrance, roughly equivalent to 0.25 miles. The neighborhood boundary was therefore taken to be the same as the maximum walkable distance, 0.25 miles, and was then divided into five sub-neighborhood areas in increments of 0.05 miles for the purposes of this research. Previous studies have usually selected target areas based on their distance from a subject building by drawing a series of concentric rings at steadily increasing distances out from the central subject building [49, 50]. However, Pollakowski and Wachter [51] took an alternative approach, instead basing the measurements of the spillover effect on the distance from a subject building to a target boundary by drawing concentric doughnuts. Figure 1 illustrates the difference between these two approaches.

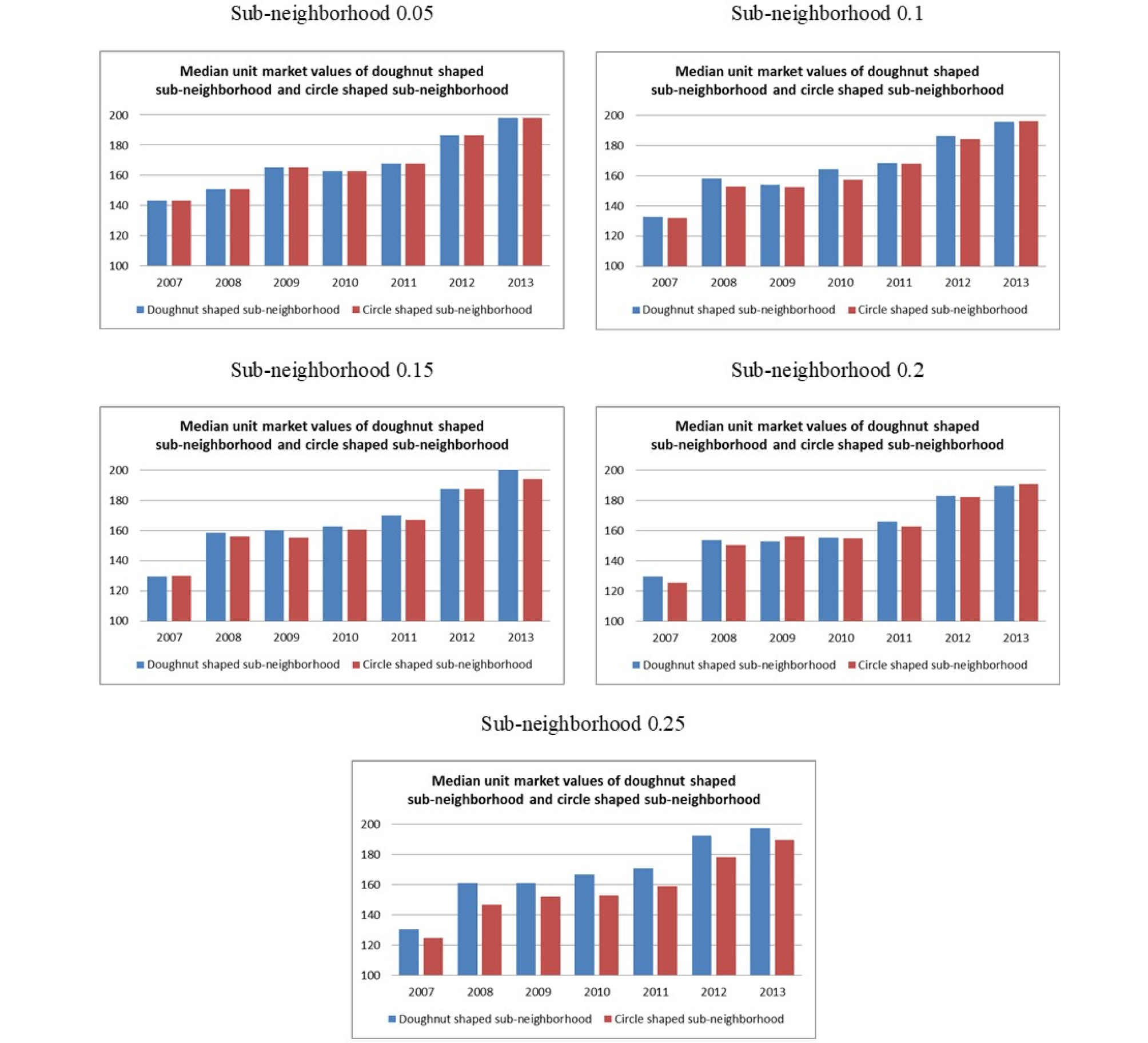

The use of concentric doughnut-shaped sub-neighborhood to calculate the median values of buildings in urban areas avoids problems due to overlapping market values for the median market values in each sub-neighborhood. The sub-neighborhood areas were selected by drawing five concentric doughnuts around each LEED and/or Energy Star certified office building to avoid the multiple counting of buildings. Interestingly, there was little difference between the median unit market values of concentric doughnut-shaped sub-neighborhoods and concentric ring- shaped sub-neighborhoods, with the trend in both types of sub-neighborhoods being similar over time. Figure 2 shows the difference in the median unit market values between the concentric doughnut-shaped sub-neighborhoods and the concentric ring-shaped sub-neighborhoods for FY 2007 through 2013.

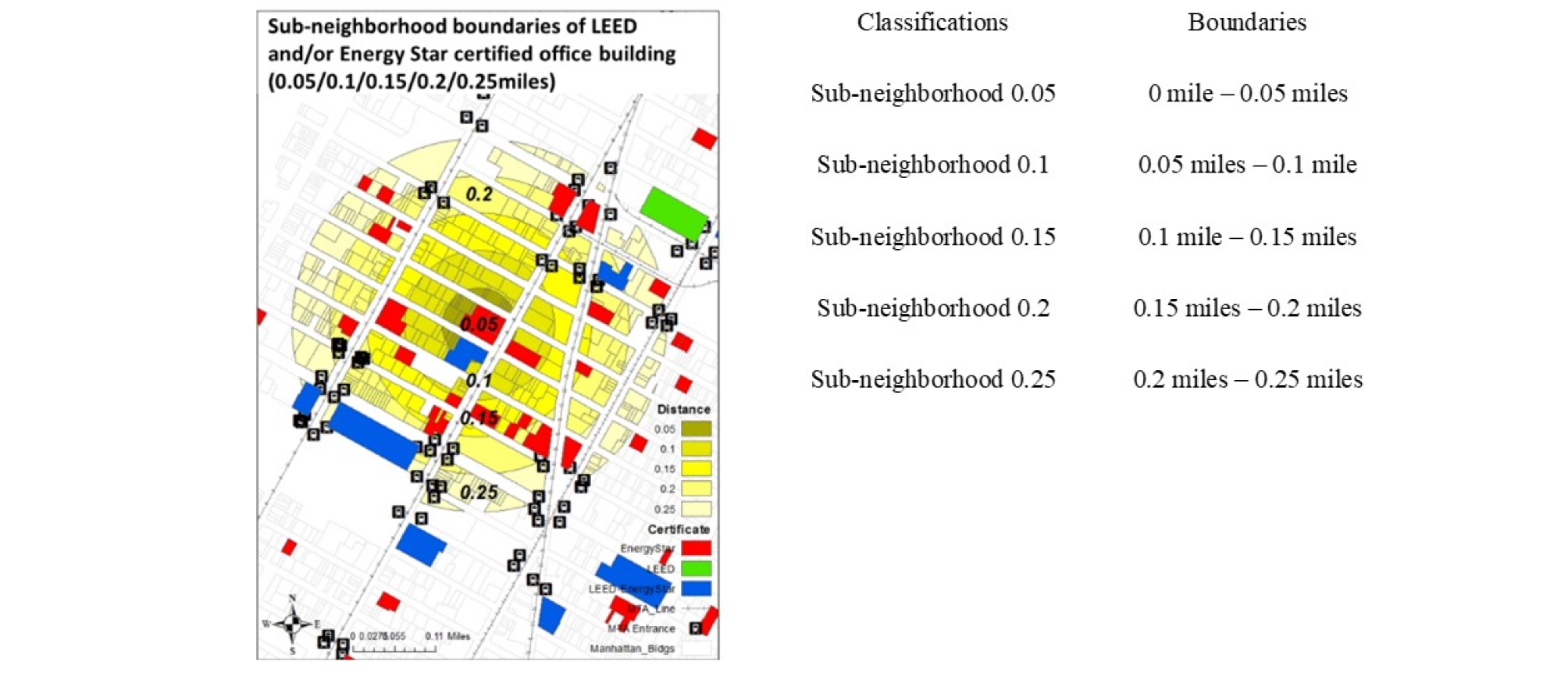

This research was based on five concentric doughnut-shaped sub-neighborhoods to enhance the accuracy and quality of the median unit market value of buildings in the sub-neighborhood of each LEED and/or Energy Star certified office building. Figure 3 shows an example of the classifications of the sub-neighborhoods, with different boundaries for each sub-neighborhood and the building distribution status for each sub-neighborhood.

Redefining sub-neighboring buildings for the median market value of the buildings in each sub-neighborhood

A building located on the boundary line between two sub-neighborhoods for a LEED and/or Energy Star certified office building, such as the boundary line between the 0.05 and 0.1 sub-neighborhoods was included in the data for both sub-neighborhoods. The unit market value of this building was counted in both sub-neighborhoods when calculating the median unit market value of buildings because this was more appropriate for the objectives of the study. A few LEED and/or Energy Star certified office buildings were included in the sub-neighborhoods of other LEED and/or Energy Star certified office buildings as a nearby building. A guiding assumption of this study was that the median unit market value of buildings in the sub-neighborhoods of each LEED and/or Energy Star certified office building would not have a significant impact on the results given the relatively limited number of office buildings that have achieved LEED and/or Energy Star certification. Again, the focus was not the individual unit market values of each sub-neighboring building. The median unit market value is, by its nature, insensitive to changes in the unit market value of individual buildings and to outliers [52]. Therefore, the median unit market value of buildings for each sub-neighborhood included the unit market values of LEED and/or Energy Star certified office buildings that fell within the sub-neighborhoods of other LEED and/or Energy Star certified office buildings when the median market value of buildings in each sub-neighborhood were calculated.

Overlapping areas of each sub-neighborhood of LEED and/or Energy Star certified office buildings

The high density of LEED and/or Energy Star certified office buildings in the midtown and downtown of Manhattan and the relatively close distances between LEED and/or Energy Star certified office buildings generated numerous overlapping areas between the sub-neighborhoods of certified office buildings. The example of overlapping areas of sub-neighborhoods of two Energy Star certified office buildings shown in Figure 4 reveals ten areas of overlap, with each overlapping area representing two different sub-neighborhood radii, one from each of the Energy Star certified office buildings. The buildings located in these overlapping areas will be affected by different economic impacts from having two Energy Star certified office buildings close by. For the purposes of this study, the economic impacts of the LEED and/or Energy Star certified office buildings were assumed to be independent of each other and the overlapping areas of sub-neighborhoods of LEED and/or Energy Star certified office buildings was identified as a limitation of the statistical research model.

The proximity to a subway entrance for each building in the sub-neighborhoods

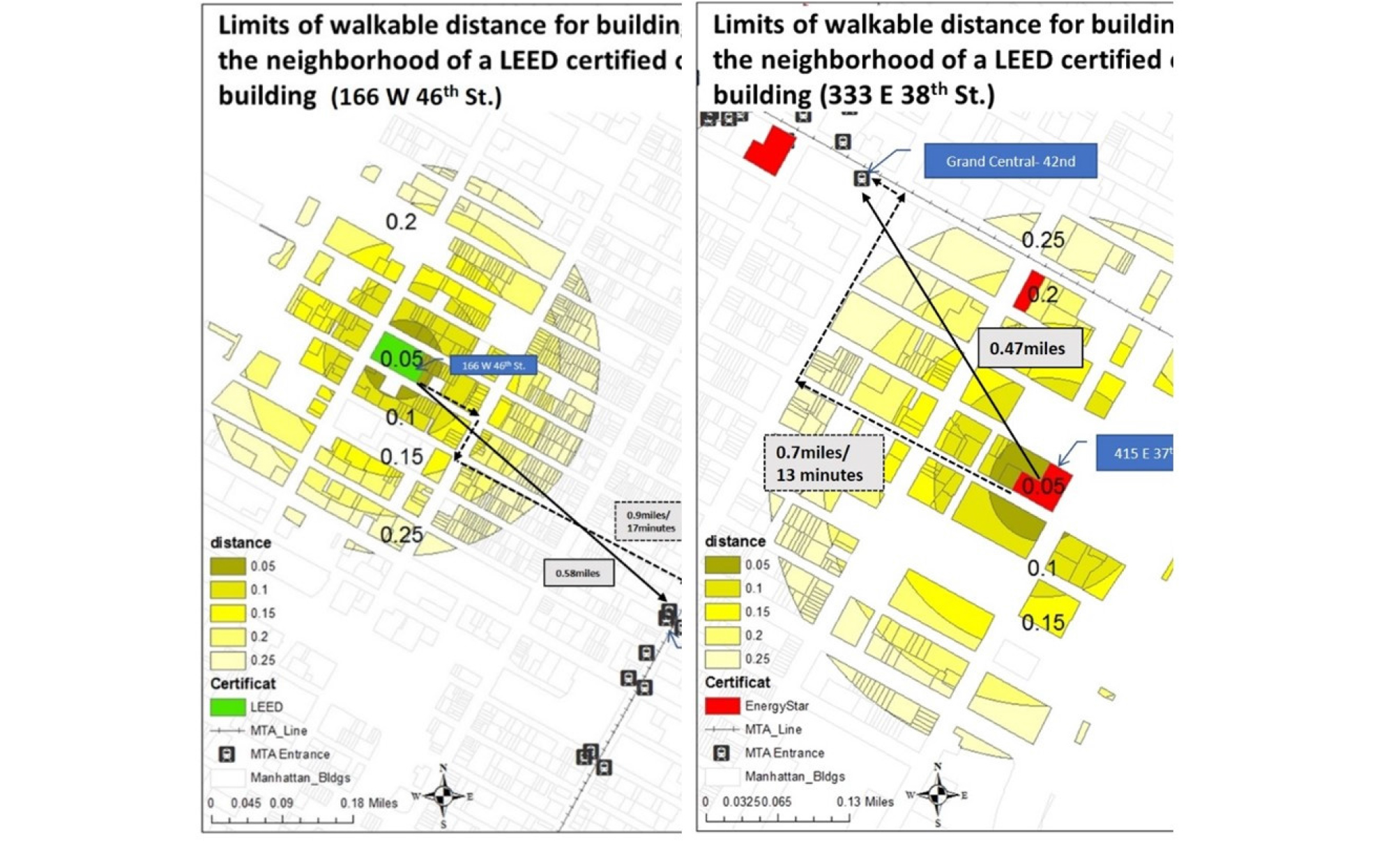

The proximity to a subway entrance could serve as a homogenous economic situation in terms of the market value of the buildings in the sub-neighborhoods because all provided equivalently convenient accessibility to the metropolitan subway transportation system and thus conveyed similar satisfaction for subway transit commuters. Also, NYC MTA has stated that any subway entrances in Manhattan can be reached within a 15-minute walk from any geographical point, which is a source of considerable satisfaction for commuters [48]. A building’s neighborhood area was thus taken to be a circle with a radius equal to the walkable distance, 0.25 miles, from the building of interest when measuring the spillover effect of a LEED and/or Energy Star certified office building on the median unit market value of buildings in its sub-neighborhood areas. Only one LEED and one Energy Star certified office building did not include a single subway entrance within their sub-neighborhood boundaries. Figure 5 presents both measurement methods for distance, pedestrian walk route distance and straight-line distance, to the closest subway entrance from each certified office building.

Findings

Geographical results

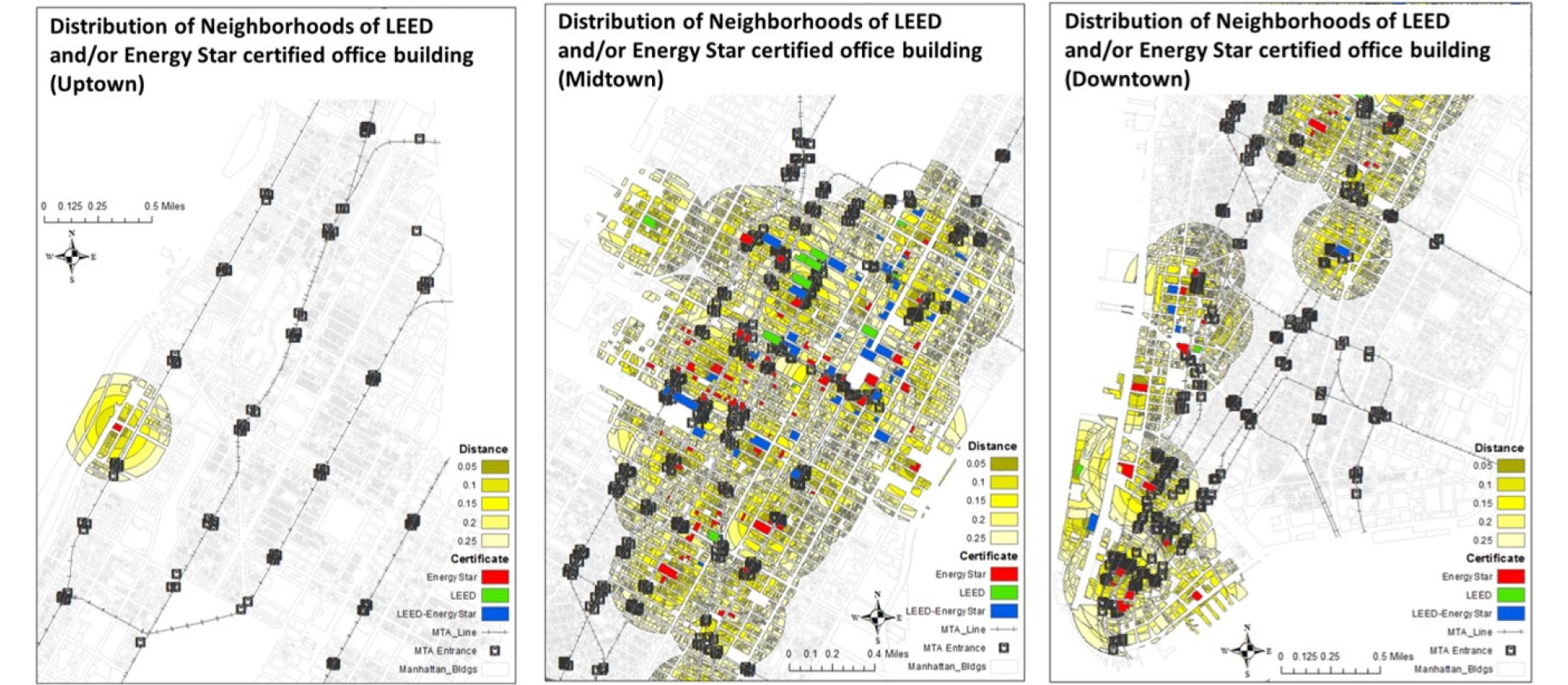

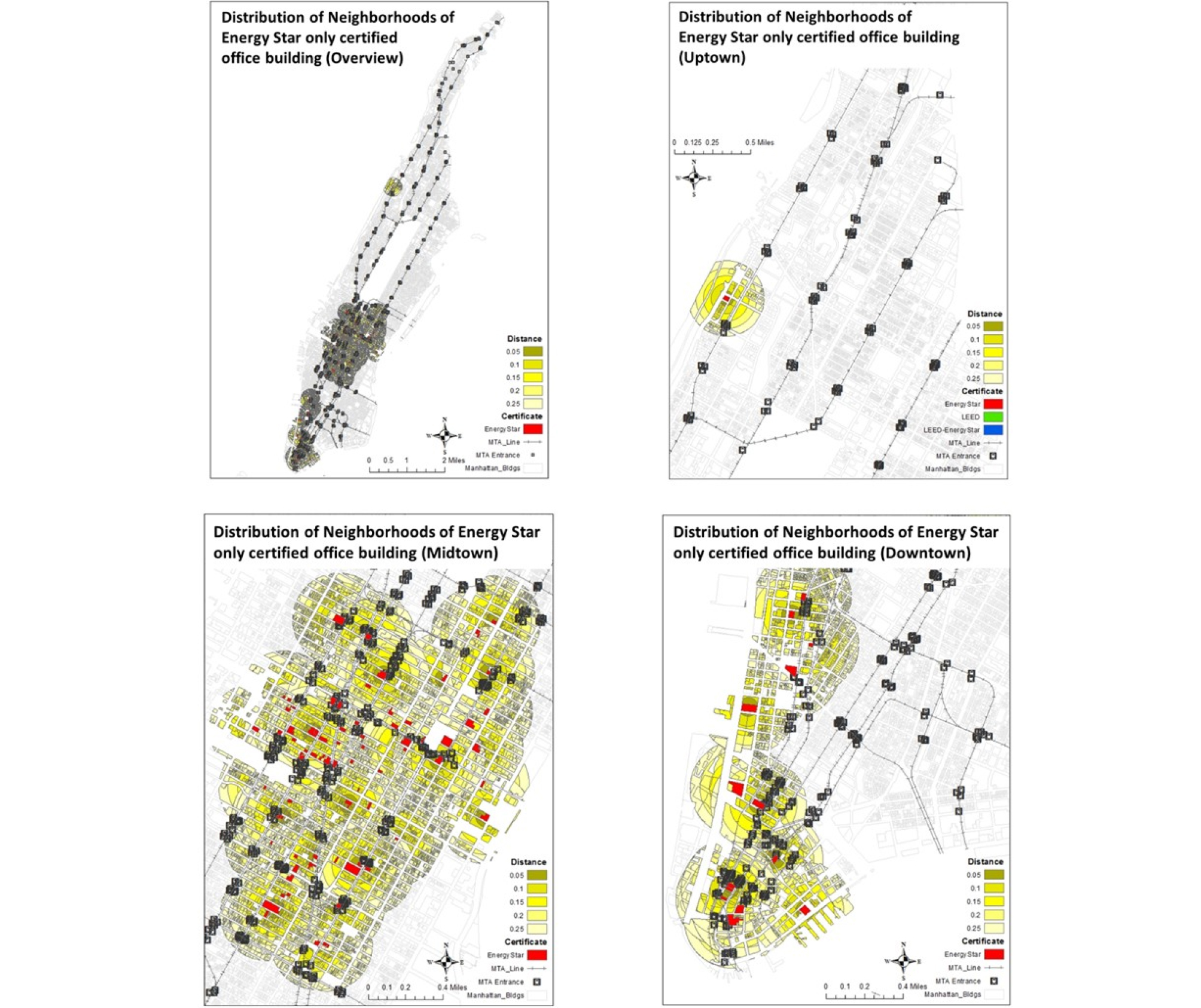

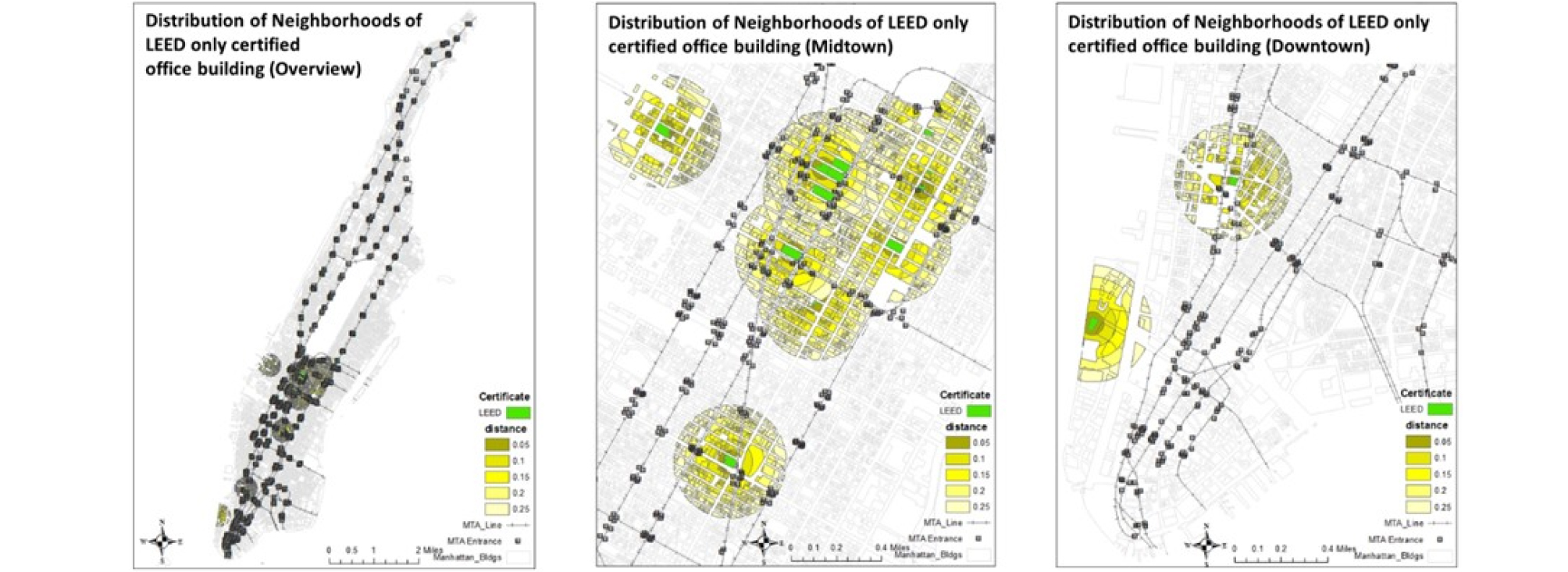

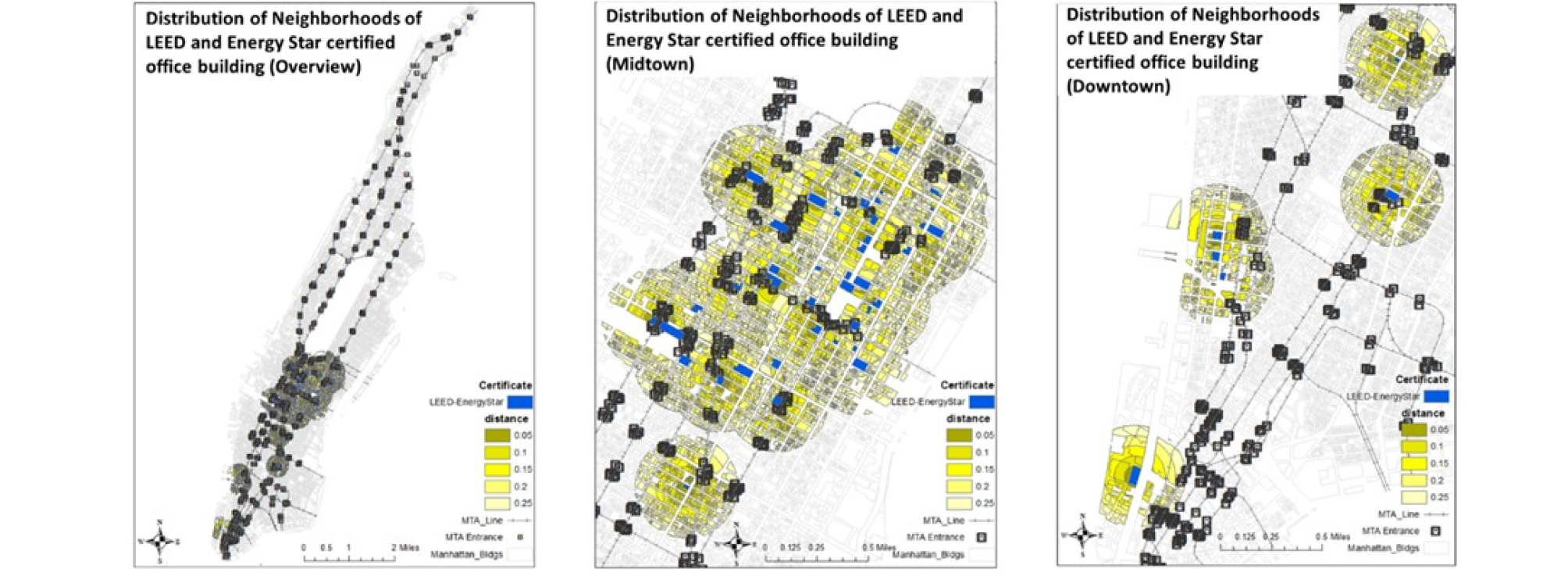

A geographical approach was used to integrate the numerical data and select the sample group [53]. In addition to determining the distribution of LEED and/or Energy Star certified office buildings and those of buildings in their sub-neighborhoods in Manhattan, NYC, individual buildings were distinguished within each different sub-neighborhood area. The market value data were added to the physical building information by matching the Borough-Block-Lot (BBL) number of every building. The number of LEED and/or Energy Star certified office buildings in Manhattan are shown in Table 4, and Figure 6 shows the distribution of these buildings and their sub-neighborhoods in detail for the three regions of Manhattan: Uptown, Midtown and Downtown.

Table 4.

Number of LEED and/or Energy Star certified office building

| LEED certification only | Energy Star certification only | LEED & Energy Star certifications | Total |

| 14 | 89 | 46 | 149 |

| 9.4% | 59.7% | 30.9% | 100% |

The number of office buildings in Manhattan within the designated sub-neighborhood areas of LEED and/or Energy Star certified office buildings was 77,530, which exceeds the actual total number of buildings included in the study because individual buildings could be included in the neighborhoods of more than one LEED and/or Energy Star certified office building. A LEED and/or Energy Star certified office building could also count as a building in the sub-neighborhood of another certified building. The number of buildings within each sub-neighborhood boundary for each certification type is shown in Table 5.

Table 5.

Number of buildings in each sub-neighborhood

The distributions of buildings in all sub-neighborhoods of each type of certified office building are presented in Figures 7 to 9.

Statistical approaches

A descriptive analysis and a regression analysis were applied to the numerical data sets exported from the results of the earlier geographical approach. The descriptive analysis examined the trends in the numerical data sets in terms of fundamental statistical values, and the regression approach looked at the correlations between pairs of independent and dependent variables to determine the significance level and the strength of the correlation.

Descriptive analysis

The first step in the descriptive analysis was to determine the number of certified buildings with each level of LEED certification coverage and certification level and the number of buildings achieving Energy Star certification from FY 2007 through 2013. Most of the office buildings that were originally LEED certified for only part of the building went on to achieve LEED certification for the whole building. Fifteen of the sixty LEED certified office buildings achieved LEED certifications at least twice for part or whole of the building. Interestingly, only two LEED certified office buildings achieved the highest LEED certification level, Platinum, for their building in 2013, and ten office buildings where only part of the building was originally certified subsequently re-achieved LEED certification for the whole building. Also, three office buildings that had already achieved LEED certification for part of the building gained another LEED certification for the whole building to upgrade the coverage of their LEED certification and another three that had already achieved LEED certification for the whole building upgraded their LEED certification to a higher certification level (Tables 6 and 7). Table 8 shows the trends in office building Energy Star certifications annually. The number of certifications tended to increase after 2007, but then dropped from 78 in 2012 to 66 in 2013; the number of Energy Star certification renewals also decreased by 12 compared with the previous year. The Energy Star certification requirements changed in 2012, which might partly explain the major drop-off the following year.

Table 6.

The number of LEED only or LEED and Energy Star certified office buildings by LEED certification coverage

Table 7.

The number of buildings with each LEED certification level

Table 8.

The number of buildings achieving Energy Star certification

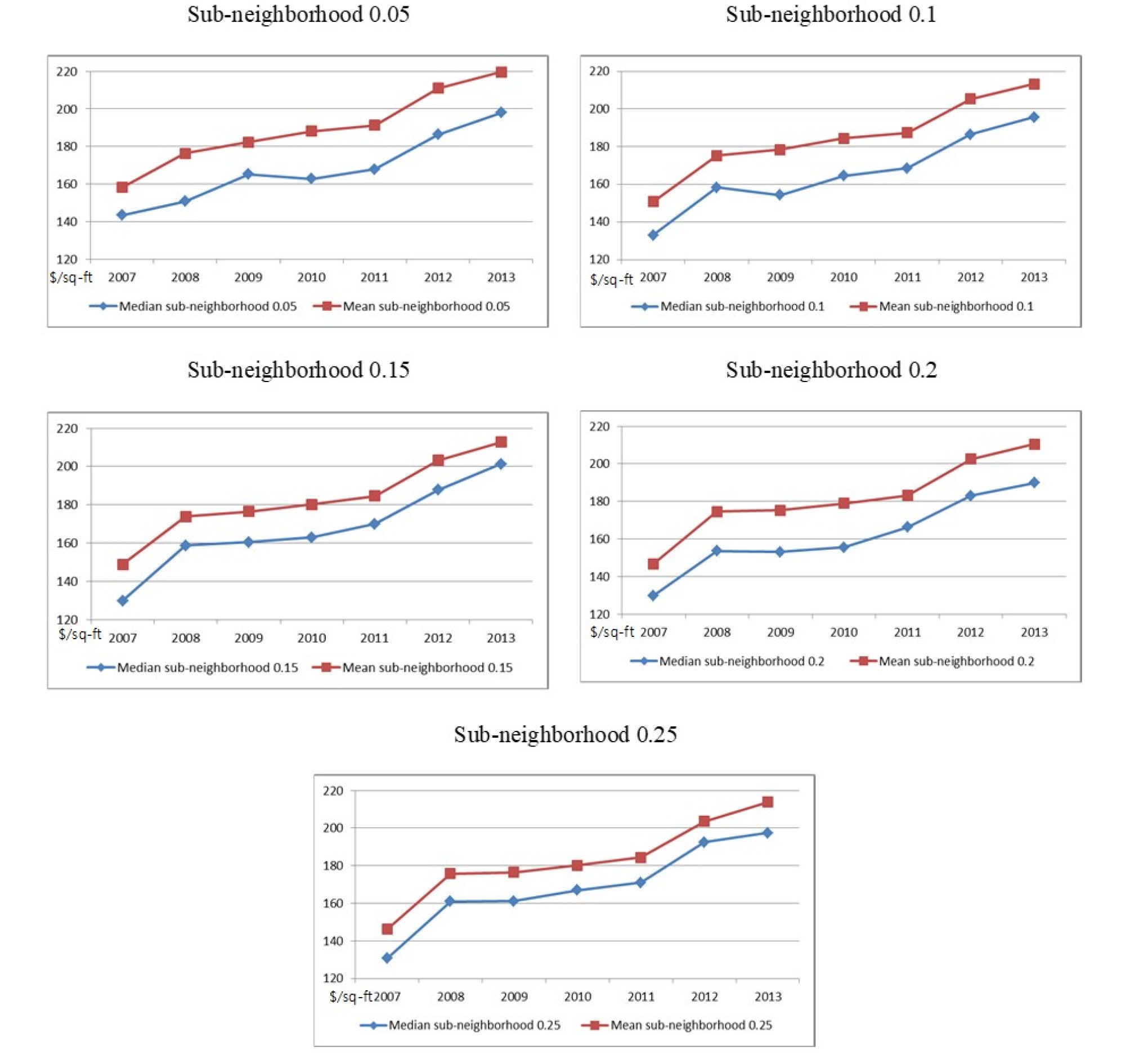

The descriptive analysis also provided a useful summary of the changes in the median unit market values of all the sub-neighborhoods surrounding the LEED and/or Energy Star certified office buildings in the study, focusing on five values: the minimum and the maximum values, the mean and the median values, and the standard deviation. The median values and the mean values from 2007 through 2013 exhibit very similar unit market price patterns for all the sub-neighborhoods, and the mean values for all the sub-neighborhoods over time were consistently higher than the corresponding median values (Figure 10).

Regression analysis

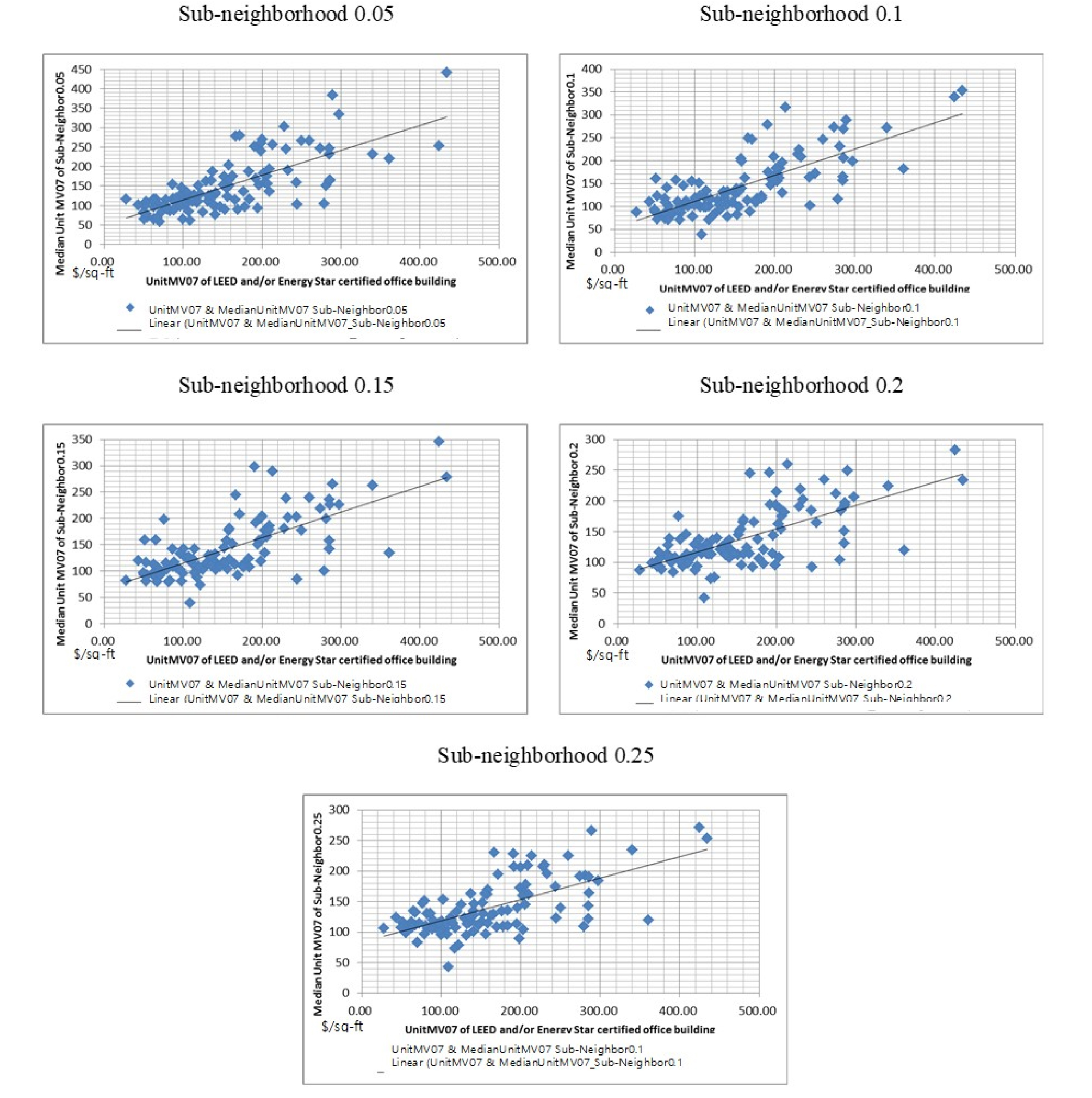

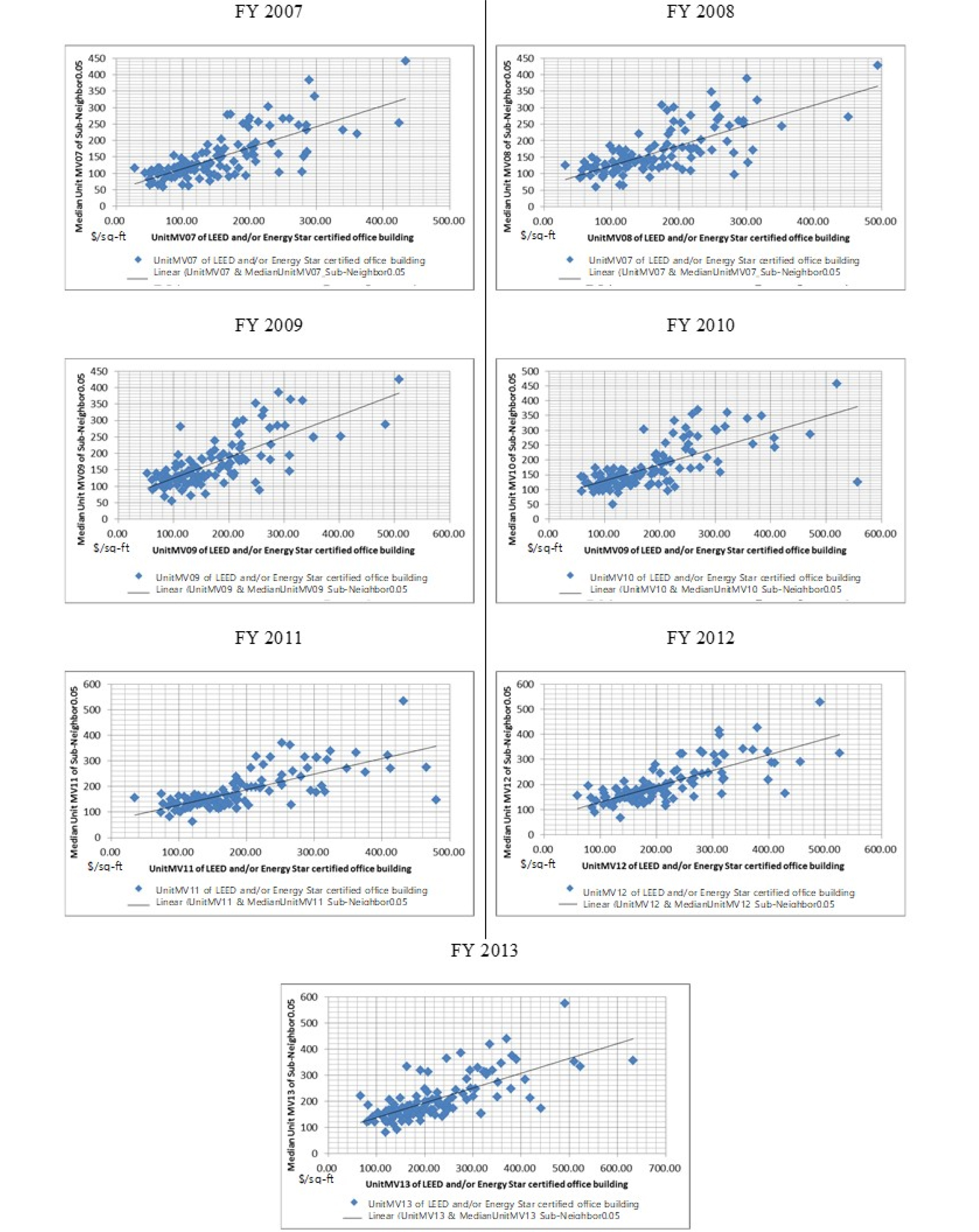

The correlation between the unit market values of the LEED and/or Energy Star certified office buildings and the median unit market values of the buildings in the five sub-neighborhoods surrounding them was examined to reveal any pattern between the two variables and identify an appropriate statistical approach model, either linear or non-linear, for the further regression process. The results of the correlation between the two variables indicated a linear correlation for both over the five different sub-neighborhoods and seven research years (Figures 11 and 12).

Based on the linear correlation between the unit market value of a LEED and/or Energy Star certified office building and the median unit market value of buildings in the five surrounding sub-neighborhoods over the seven year study period, there was indeed a correlation between the median unit market value of buildings in each radius neighborhood and that of the LEED and/or Energy Star certified office building. Moreover, this correlation could create spillover effects, in terms of both strength and direction, on the median unit market value in each sub-neighborhood through the coefficients in the regression result. Two regression models were utilized; the hedonic price model selected the most appropriate linear equation and the LMEM indicated the significance of variables and the strength and direction of the correlation between the dependent variable and the independent variable. Five results were developed for the hedonic price model and five for the LMEM.

R2 values of sub-neighborhoods of LEED and/or Energy Star certified office buildings

The correlation between the unit market value of a LEED and/or Energy Star certified office building and the median unit market value of buildings in sub-neighborhood 0.05 is 0.715. The model for this sub-neighborhood does not need to transform the values from the linear equation to any of the other equation options because there was no substantial difference with respect to the correlation or the coefficient determined by the R2 value for the linear and log-log equations. The R2 values for the remaining sub-neighborhoods indicated that the linear hedonic price model equation was more appropriate than the other hedonic price model equations. The further regression processes were therefore based on the linear hedonic price model equation without any transformations (Table 9).

Table 9.

R2 values for the four hedonic price model equation options

The LMEM is based on the linear hedonic price model equation, which indicates that the data sets for the dependent and independent variables could be directly applied to the LMEM without the need for data transformation using natural logarithms. These LMEMs reveal the effect of a LEED and/or Energy Star certified office building on the median unit market value of buildings in each sub-neighborhood as follows:

1) LMEM for the impact of the achievement of LEED and/ or Energy Star certifications on the five sub-neighborhoods

The model equation used to examine the effect of achieving LEED and/or Energy Star certification on the median unit market value in each sub-neighborhood located from within a 0.05-mile radius out to a 0.25-mile radius of the certified building was:

where Y is the median unit market value of the buildings in each sub-neighborhood; Xunit is the unit market value of the LEED and/or Energy Star certified office building; XLEED certificationand XEnergy Star certification are independent variables; βn are the coefficients for the fixed effects; αn are the coefficients for the random effects; and prox indicates each sub-neighborhood being considered.

The results of the LMEMs for each sub-neighborhood represent the significance of the variables and the strength and the direction of the effect of the LEED and/or Energy Star certified office building in Table 10.

Table 10.

The LMEM results for the impact of a LEED and/or Energy Star certified building on the five sub- neighborhoods

The estimated coefficient of each of the independent variables in Table 10 indicates the strength and the direction of the effect of the LEED and/or Energy Star certified office building without any transformation of values; thus, all the independent variables had a positive impact on the dependent variable irrespective of the five different proximities to the LEED and/or Energy Star certified office building. The greatest impact on the unit market value of a LEED and/or Energy Star certified office building was found to be on the median unit market values in sub-neighborhood 0.05; this impact decreased sharply for sub-neighborhood 0.1 and then remained fairly constant for the sub-neighborhoods that were further out. Similarly, the strength of the impact of Energy Star certification achievement initially increased as the distance from the certified building decreased. The strength of the impact of achieving LEED certification was higher than that of achieving Energy Star certification in all sub-neighborhoods. However, it was difficult to interpret the results for the strength of the impact of LEED certification achievement because it appeared to fluctuate considerably during the research period for all sub-neighborhoods. Overall, the strength of the impact on the unit market value of a LEED and/or Energy Star certified office building and the proximity of different sub-neighborhoods were directly proportional to each other, while the strength of the impact of Energy Star certification achievement alone was inversely proportional to the proximity of neighborhood. Although the simple fact of a building achieving a LEED certification had a positive impact on the median unit market value of the buildings in all the sub-neighborhoods, it was hard to identify a strong relationship between the strength of the impact of LEED certification achievement on the median unit market value or the proximity to an office building that achieved LEED certification.

2) LMEM for the impact of different LEED certification levels on the five sub-neighborhoods

This LMEM equation analyzed the effect of LEED certification levels on the median unit market value for each sub-neighborhood based on five different proximities to LEED only or LEED and Energy Star certified office buildings. The LEED certification levels became an independent variable in this model, so the results indicate the strength of the impact of each different LEED certification level on the median unit market value in each sub-neighborhood:

where Y is the median unit market value of each sub-neighborhood; Xunit is the unit market value of the LEED only or LEED and Energy Star certified office building; XLEED certification level is an independent variable; βn are the coefficients of the fixed effects; αn are the coefficients of the random effects; and prox is the proximity to the LEED certified office buildings.

The results of the LMEMs for each sub-neighborhood are summarized in Table 11. The independent variables were significant for the median unit market values of the sub-neighborhoods, with all falling below the significance level of 0.05. Three LEED certification levels, Certified, Silver and Gold, had a positive estimated coefficient for all sub-neighborhoods, while the highest LEED certification level, Platinum, had a negative estimated coefficient for all sub-neighborhoods. The strength of the LEED certification levels exhibited a significant difference between the three LEED certification levels and the LEED Platinum level.

Table 11.

Summary of the LMEM results for the impact of LEED certification level on the five sub-neighborhoods

Although the estimated coefficient for LEED Platinum was statistically significant in this model, this was likely due to the extremely small number of buildings in the screened population (n=2). The pattern of the strength of the impact of unit market value of office buildings which achieved LEED certification on the median unit market value of each neighborhood was very similar to the pattern shown in the previous LMEM. Overall, there was a positive impact of the unit market value of an office building which achieved LEED certification for all sub-neighborhoods, but this positive impact decreased steeply from sub-neighborhood 0.1 onwards, although a small positive impact was maintained to the outer edge of sub-neighborhood 0.25.

3) LMEM for the LEED certification coverage on the five sub-neighborhoods

The LEED certification coverage indicates that a building achieved LEED certification for part or all of the building during the study period. Therefore, the median unit market value in each neighborhood containing an office building which achieved LEED certification played a role in the dependent variable and the variables related to the LEED certification itself should be an independent variable. The model equation took the following form; the results obtained with this model are shown in Table 12.

Table 12.

Summary of the LMEM results for the LEED coverage

The meaning of the mathematical symbols in this equation is the same as the previous description except for the symbol XLEED certification coverage, which signifies the portion of LEED certification in a LEED certified office building.

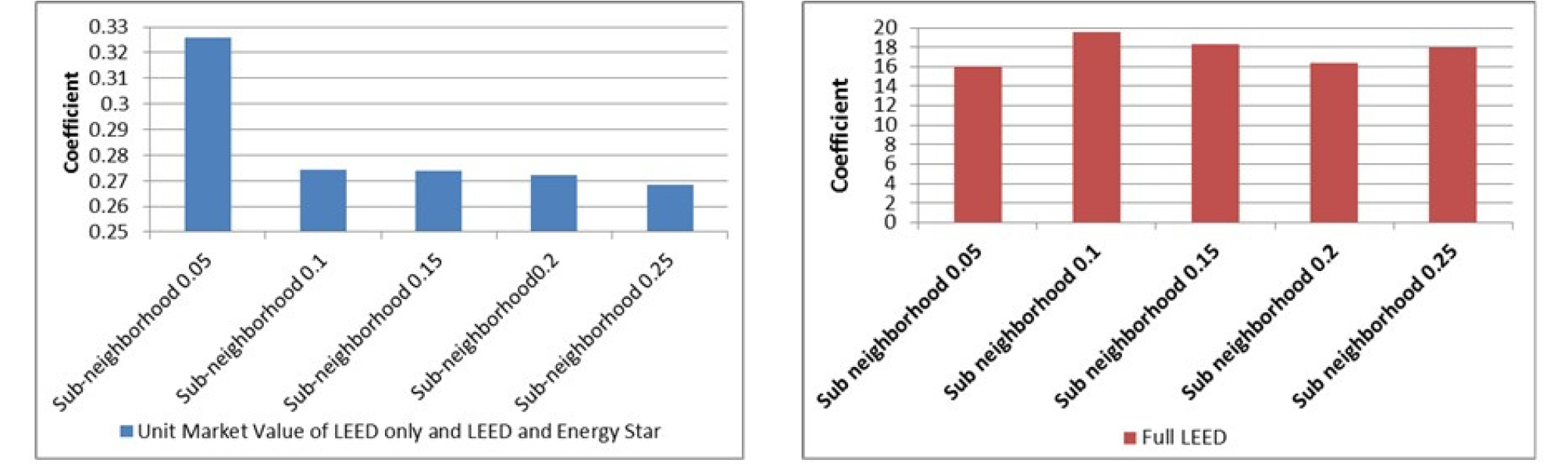

The results for each sub-neighborhood indicate that the variation in the partial LEED certification coverages was not significant for any of the sub-neighborhoods because all had p-values greater than 0.05. This is likely due to the limited number of partial LEED certified office buildings in this research area during the study period. All the other independent variables were significant, and Figure 13 shows the patterns for the strength of impact for each sub-neighborhood. The strength of the impact of the unit market value of a LEED certified office building for each sub-neighborhood again followed a similar pattern to that for the previous two models. The strongest impact on the unit market value of proximity to an office building with LEED certification was found in sub-neighborhood 0.05, with the strengths of those impacts for the remaining sub-neighborhoods being very similar. The strength of the impact of full LEED certification was between approximately 16 and 20 for all sub-neighborhoods. The highest coefficient value was for sub-neighborhood 0.1, but the lowest coefficient value was for sub-neighborhood 0.05.

Model validation

The model validation was based on the LRT to select between the fitted model and the null model by comparing the values of the AIC (Akaike Information Criterion) and BIC (Bayesian Information Criterion) for all the models. As five sub-neighborhoods were studied, each LMEM required the LRT to be performed five times to consider each of the five sub-neighborhoods for each LEED and/or Energy Star certified office building. Three model validations were thus performed for the four LMEMs between the dependent variable and the independent variables, with five LRTs for the five sub-neighborhoods. The null model was that the fitness of the fitted model would be decreased by adding variables to the fitted model, which includes only an intercept; the LRT hypotheses tested were as follows:

H0: The null model is true.

H1: The null model is not true.

The results of the LRT for each sub-neighborhood for the three model validations are shown in Table 13. All the p-values were below 0.0001, which confirms that the results were significant. The values of AIC and BIC for the fitted models for all the sub-neighborhoods were consistently smaller than the values for the null models, indicating that statistically, the fitted models were better than the null models for all the sub-neighborhoods.

Table 13.

Summary of the results of the LRT values for the three models

Conclusions

This study measured the spillover effect of LEED and/or Energy Star certified office buildings in Manhattan, NYC, on buildings in their neighborhoods based on their proximity to a certified office building. These results suggest that LEED and/or Energy Star certified office buildings were indeed correlated with an increase in the median unit market values of buildings in their surrounding neighborhoods, and the strength of the impact of the unit market value of a LEED and/or Energy Star certified office building over time on the median unit market values for successive sub-neighborhoods exhibited an inverse proportion pattern that demonstrates how this spillover effect declines with decreasing proximity to the certified office building. These findings indicate that the presence of a LEED and/or Energy Star certified office building in Manhattan and its certification level are correlated with various positive economic benefits related to the unit market values of buildings located within 0.25 miles of the certified building. LEED and/or Energy Star certified office buildings could thus play a role in encouraging mutual growth in the real estate market to satisfy part of the triple bottom line of sustainability for both the LEED and Energy Star certifications. This study provides a useful foundation for further research to identify the spillover effect of all types of LEED and/or Energy Star certified buildings to support the mutual growth of LEED and/or Energy certified office buildings and their neighborhoods from a socio-economic standpoint, representing a win-win approach. However, there are a few limitations in this research: (1) The buildings in all the sub-neighborhoods were assumed to have homogenous external features in the existing environment in terms of measuring the spillover effect of the LEED and/or Energy Star certified office building. In actuality, the market values of office properties are affected by numerous external features in the environment including economics, politics, and social science; (2) The building owners, investors, and developers are also interested in obtaining a reasonable return on investment (ROI), but this study considered only the unit market value when evaluating the economic benefits of LEED and/or Energy Star certification. Future research needs to consider the economic interests of building owners, investors, and developers, including the expense involved in achieving LEED and Energy Star certification; (3) Buildings in the same sub-neighborhood and buildings in the overlap areas between the sub-neighborhoods of multiple certified buildings were assumed to experience the same impact due to the LEED and/or Energy Star certified office buildings in this study. If the impact of a LEED and/or Energy Star certified office building was to be measured individually for a particular building in a sub-neighborhood, the sub-neighborhoods and the overlap areas must be distinguished to achieve the expected outcomes; and (4) Only two of the office buildings achieved LEED Platinum level for the whole building or any levels of LEED for part of the building in the screened population, so confidence in the statistical results for both variables is inevitably constrained with regard to accepting their statistical significance. The number of both types of certified office buildings should be increased by extending the study to additional comparable research areas or expanding the research period to achieve statistical significance.